Before you start:

- IRS Regulations changed effective January 1st, 2018. A like-kind exchange, or 1031 exchange, can only be completed for real property. See here for more details.

- A like-kind exchange consists of three main steps. All three steps must be completed for the tax return to contain the correct information.

Step 1: Disposing of the original asset

- Open the Asset Entry Worksheet for the asset being traded.

- Scroll down to the Dispositions section.

- In the Date of disposition field, enter the date the property was given up.

- Do not complete any other information in the Dispositions section. Entering other information, such as sales price, will generate the Form 4797.

Step 2: Completing the 8824

- Open the 8824.

- In the Form 8824 General Information Smart Worksheet complete lines A-C.

- In Part I complete lines 1-7 with the applicable trade information.

- Complete the Summary Smart Worksheet:

- Lines A-F will pertain to the property received.

- Lines G-K will pertain to the property given up.

- If no additional property was given up leave like J blank. Entering a 0 will result in the need to enter data in the Additional Information Regarding UNLIKE-Kind Property Given Up Smart Worksheet.

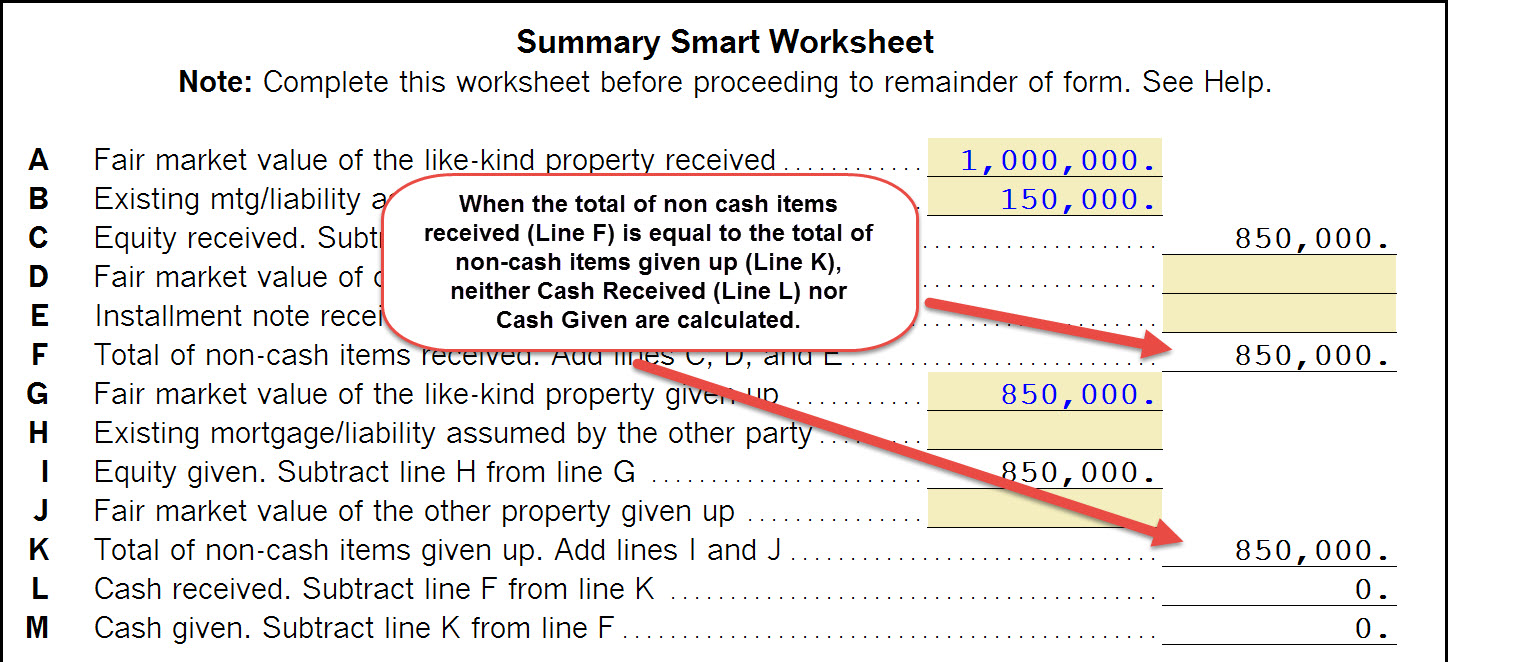

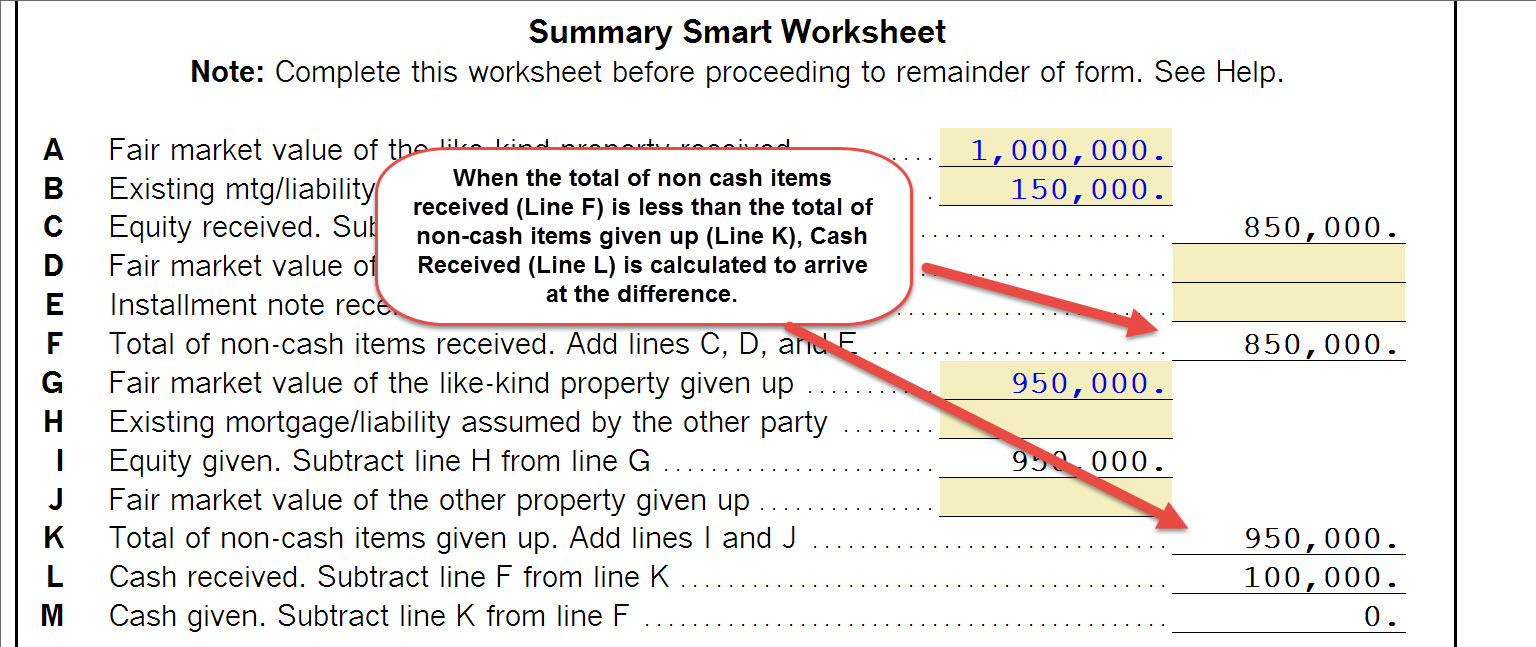

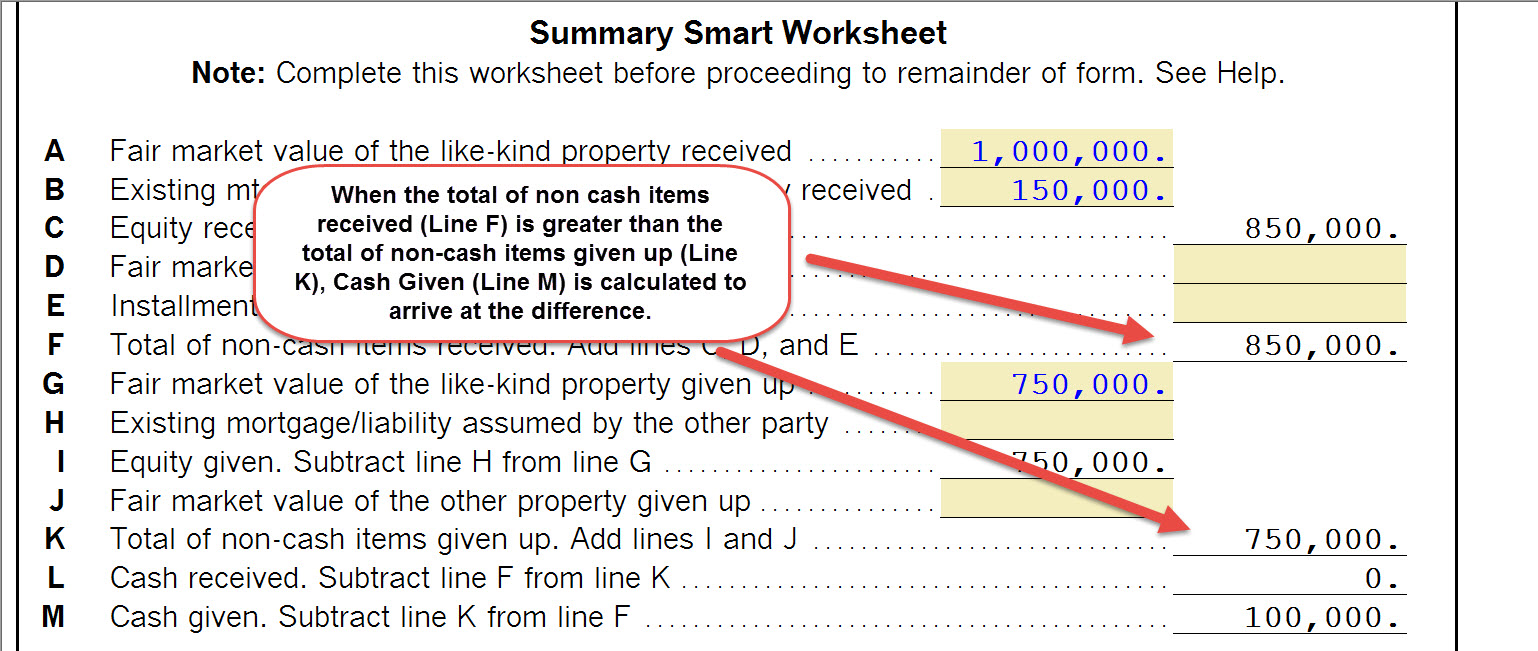

Click here to see visual examples of a completed Summary Smart Worksheet

Example of the Summary Smart Worksheet for an even exchange:

Example of the Summary Smart Worksheet for an exchange with Cash Received:

Example of the Summary Smart Worksheet for an exchange with Cash Given:

- Complete the Additional Information Regarding Like-Kind Property Given Up section lines N through T.

- If Line J contains a value the Additional Information Regarding UNLIKE-Kind Property Given Up Smart Worksheet will activate and require entries. Complete these if Unlike property was given up.

- ProSeries will now flow these entries to the 8824 to complete the required calculations. There are some important lines to review:

- Line 23 is the amount of gain, if any, that will be taxable on the tax return.

- Line 25 is the Basis of like-kind property received. You'll need this for Step 3.

- The Replacement Property Depreciable Basis Components Smart Worksheet will show the Exchanged (carryover) basis and the Excess (additional) basis for both regular tax and AMT. You'll need these for Step 3.

Step 3: Entering the new asset entry worksheet(s)

Before you create the new asset, you'll need to decide if you're electing out of the regs in IRC Section 1.168(i)-6(i). If you are electing out of the regs then only one new asset entry worksheet is needed. If you elect to use the regs then you'll need multiple asset entry worksheets (one to track excess basis and one to track exchange basis). Complete the appropriate Step 3 for your choice:

![]() The first asset containing the Exchanged basis Section 179 cannot be claimed but Special Depreciation Allowance may be claimed if eligible. The second asset containing the Excess basis both Section 179 and Special Depreciation Allowance may be claimed if eligible.

The first asset containing the Exchanged basis Section 179 cannot be claimed but Special Depreciation Allowance may be claimed if eligible. The second asset containing the Excess basis both Section 179 and Special Depreciation Allowance may be claimed if eligible.

Completing a like-kind exchange of vehicles in a 1040 return for ProSeries 2017 and prior

- Open the Car and Truck Expenses Worksheet of the vehicle you wish to dispose of.

- Enter a date of disposition on Line 47 to stop depreciation as of the date of the exchange (Vehicle Expenses Worksheet for Form 2106, Line 41).

![]() Don't enter a sales price. Entering a sales price, even a zero, forces the program to assume there's no exchange occurring. The program will then calculate a gain or loss as if a normal sale occurred.

Don't enter a sales price. Entering a sales price, even a zero, forces the program to assume there's no exchange occurring. The program will then calculate a gain or loss as if a normal sale occurred.

- Double click on Line 53a to link this vehicle to Form 8824.

- If necessary, enter amounts on Lines 53b and 53c.

- Open Form 8824.

- Complete all applicable fields on Form 8824.

- Open the Car and Truck Expenses Worksheet (Vehicle Expenses Worksheet for Form 2106).

- Add the newly received vehicle in the next available column (create a new copy of the worksheet if necessary). Use the figure from Form 8824, Line 25 in determining the cost or basis on Line 30.