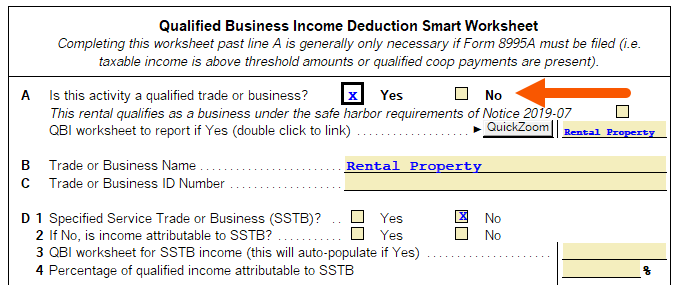

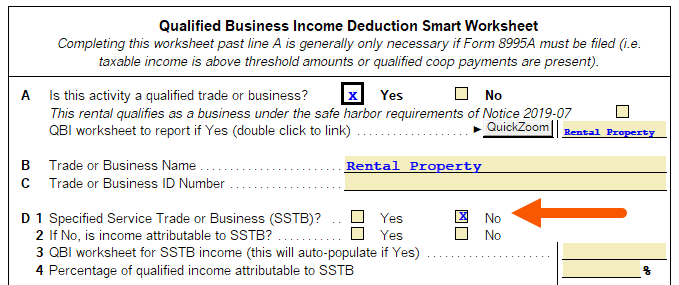

The Tax Cuts and Jobs Act adds a new deduction for non-corporate taxpayers for qualified business income. The deduction is intended to reduce the tax rate on qualified business income to a rate that is closer to the new corporate tax rate.

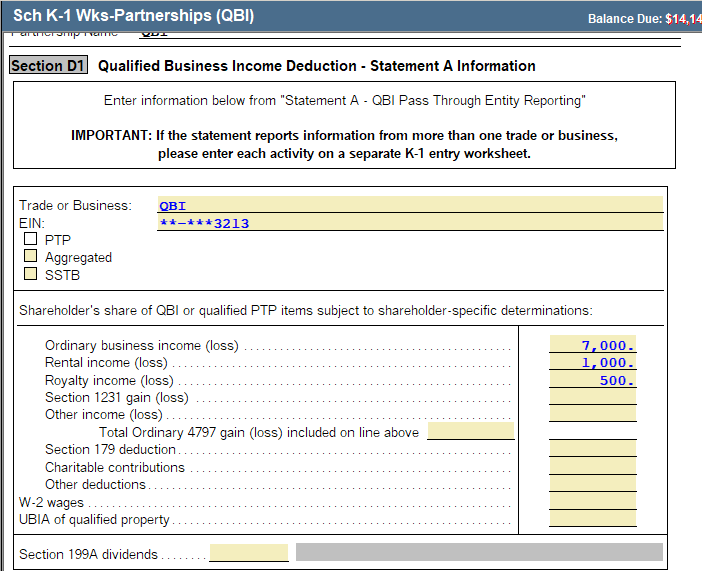

It reduces the less of taxable income or business income and is generally 20% of a taxpayer's qualified business income (QBI) from a Partnership, S-Corporation, or Sole Proprietorship, defined as the net amount of items of income, gain(s), deduction(s), and loss with respect to the trade or business. Certain types of investment-related items are excluded from QBI, including capital gains or losses, dividends, and interest income (unless the interest is properly allocable to the business).

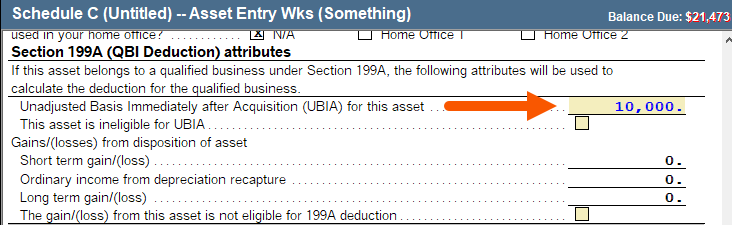

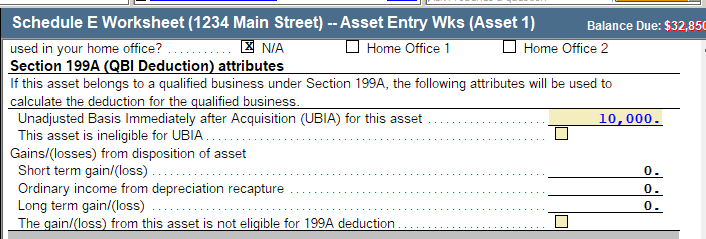

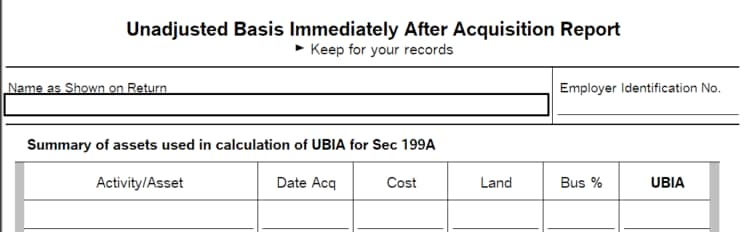

Taxpayers whose taxable income exceeds the threshold amount of $157,500 ($315,000 in the case of a joint return) are subject to limitations based on the W-2 wages and the unadjusted basis in acquired qualified property.

When the taxable income is more than $157,500 but not more than $207,500 ($315,000 and $415,000 if married filing jointly), the computed 20% deduction amount will be partially limited to the higher of 50% of wages paid by the business, or 25% of the wages paid plus 2.5% of the unadjusted basis of qualified property. If the business has no wages paid, and no qualified property, a partial deduction will be allowed.

The deduction is taken for partnerships and S-Corporations at the partner or shareholder level. Trusts and estates are eligible for the deduction. W-2 wages and the unadjusted basis in acquired qualified property are apportioned between the trust or estate and the beneficiaries.

Specified agricultural or horticultural cooperatives are also eligible for the deduction under special rules. Qualified business income includes only income effectively connected with a U.S. trade or business (or Puerto Rico if all the income is subject to U.S. tax).